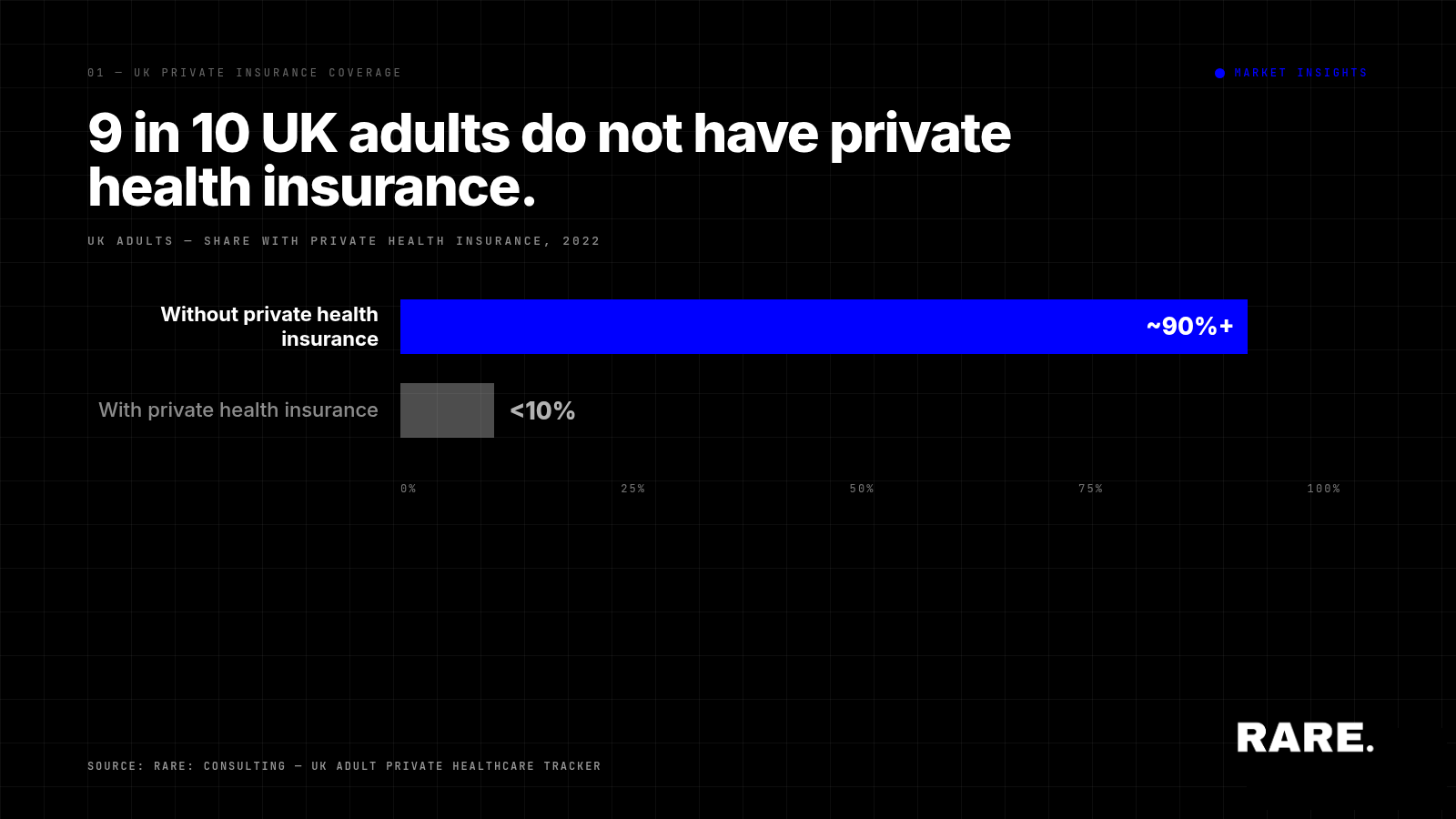

The last two years have seen a shift in behaviours across a variety of sectors, and healthcare is no different. An industry that was midway through a mainly technological shift in behaviours has accelerated at a pace beyond initial expectations in several areas, with the pandemic playing its part in encouraging the adoption of new behaviours, and the desire to be safer in general.

The UK healthcare sector enters 2022 having compressed years of behavioural change into 24 months. The pandemic accelerated the adoption of remote-first care, surfaced a parallel mental health crisis, and pushed wearable health technology from a fitness category into a clinical one. Each of those shifts is now structural rather than temporary, and the commercial implications for healthcare providers, manufacturers and policymakers run through the next several years of UK health planning.

Why has telemedicine moved faster than anyone expected?

The shift to digital care delivery was already happening before COVID-19. The pandemic forced it into an entirely different timeline. Routine GP appointments that would have taken five years to migrate to telehealth made the move in five months. Specialist consultations followed. Triage, diagnostics and follow-up care are all increasingly running through digital channels, and patient acceptance of those channels has held even after lockdowns ended.

The benefit to non-urgent care is significant. Patients avoid the trip to a GP surgery or A&E for problems that can be assessed remotely. The benefit to providers is faster patient throughput, lower facility costs, and access to patients across geographic boundaries that previously constrained their practice. Some patient populations, particularly the elderly, the digitally excluded, and those with complex chronic conditions, still need in-person care. But the default for non-urgent contact has moved.

The next planning question for UK healthcare is whether centralised non-urgent triage at NHS24 level becomes the entry point to GP services. The NHS is under significant staffing and waiting-list pressure, and consolidated remote triage is one of the few interventions that scales without proportional staff cost increase. The infrastructure is not there yet. The direction of travel is.

How big is the post-pandemic UK mental health pressure?

Depression rates in the UK have doubled since the start of the pandemic, according to ONS data. The increase has fallen disproportionately on already-vulnerable groups: young people, women, clinically vulnerable adults, disabled people, and those living in the most deprived UK communities. Inequality has widened, and the consequences are now visible in clinical demand for mental health support.

Despite the rise in depression, GP-led mental health diagnoses fell by almost a quarter over the same period. The implication is not that fewer people need help. It is that fewer people are reaching the help they need. Access to mental health care is in measurable decline at the same time the underlying demand is rising. The gap is being filled, partially, by private mental health providers, online support communities, mindfulness and wellbeing apps, and peer support programmes. Each of those routes has different clinical robustness and different commercial sustainability.

For policy, the question is how to scale access without adding a UK-wide funding commitment that the Treasury is unlikely to support short-term. For private healthcare providers, the question is whether to enter the mental health space directly or partner with established mental health platforms. For employers, the question is whether structured mental health support becomes a workplace benefit category. The answers shape the next several years of UK mental health provision.

What is wearable health technology actually doing in 2022?

Wearable health tech has crossed from a fitness adjacency into clinical infrastructure. The category was worth around $30 billion globally before the pandemic. By 2027, it is forecast to reach $200 billion, an unusually steep growth curve that reflects both consumer adoption and clinical integration. The number of wearable health tech devices in active use globally crossed one billion during 2022.

The clinical applications are widening. Diabetes monitoring, asthma tracking, atrial fibrillation detection, sleep apnoea monitoring, and post-operative recovery measurement are all now running on wearable platforms in the UK. The integration with patient records is the next layer. Where wearable data flows into the clinician's view of the patient, the device is no longer a consumer product. It is a clinical input.

For UK private healthcare providers, the practical question is whether to integrate wearable data into the patient record and treatment planning, and at what scale. Providers that integrate well will offer continuous-care models that are commercially sticky. Providers that ignore the wearable layer will continue to compete on episodic-treatment economics that are getting harder. The 2022 trend curve points firmly at the integration side.