Licensing reform will shrink the UK aesthetics provider base by up to 25%, accelerate consolidation, and force every manufacturer to rethink territory plans. The commercial teams that plan now will have a six-month head start.

The UK medical aesthetics market is about to hit a wall that most commercial plans haven't accounted for. Licensing regulation — long discussed, now inevitable — will fundamentally change who can offer treatments, where they can offer them, and how manufacturers reach them.

This is not a compliance story. It is a commercial one.

The current landscape is built on fragmentation

The UK aesthetics market has grown on the back of low barriers to entry. Anyone with a short training course can set up a clinic and start injecting. The result: thousands of independent operators, a patchwork of quality, and a commercial model built around volume — more reps, more territory, more accounts.

That model works when the market is expanding and regulation is light. It stops working the moment licensing changes who is allowed to practise.

What licensing reform actually means for commercial teams

The direction of travel is clear. Government consultations, industry bodies, and insurers are converging on a licensing framework that will require practitioners to meet minimum qualification standards, operate from registered premises, and submit to inspection.

Three things change overnight when this lands:

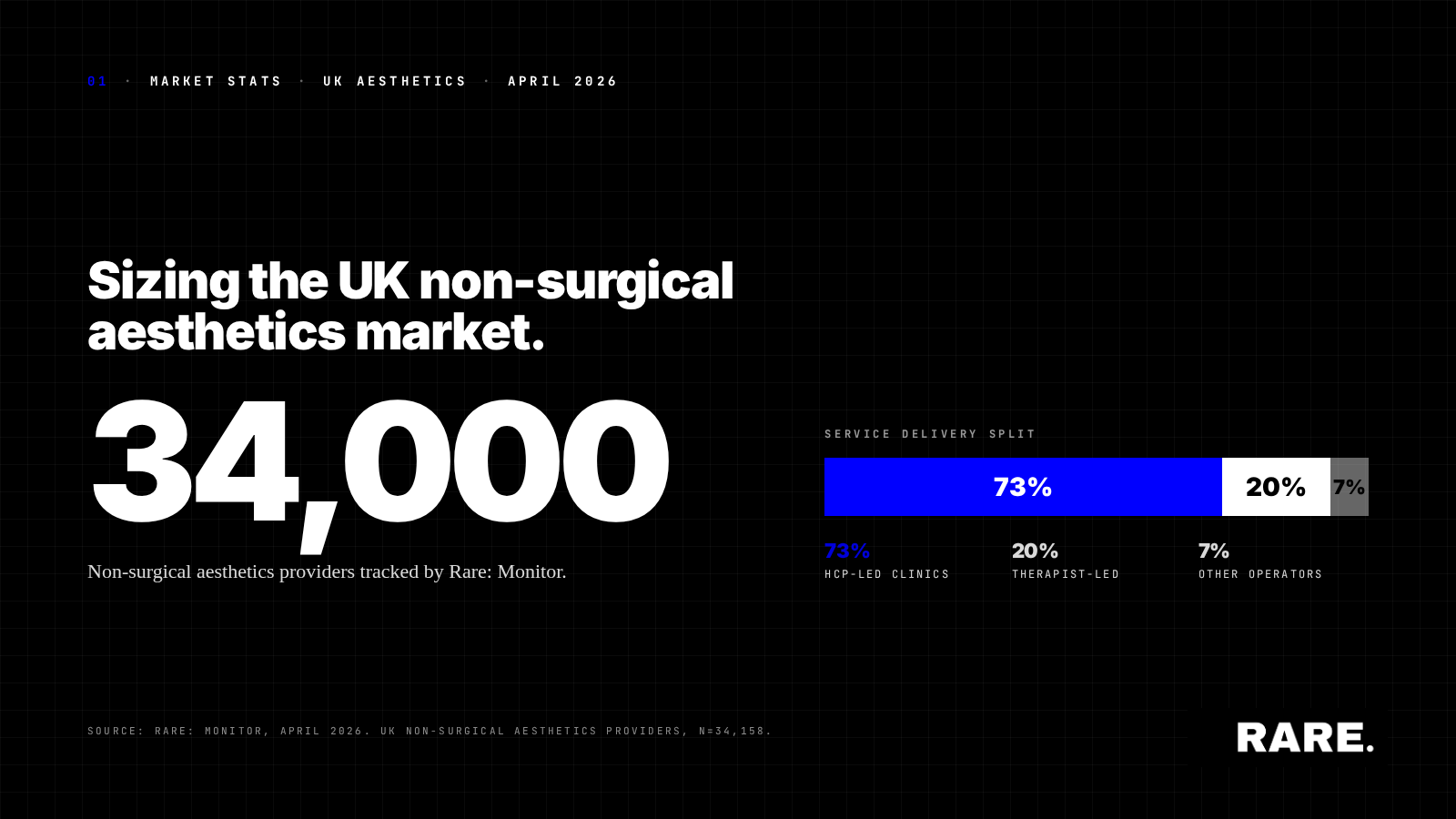

The provider base shrinks. Operators who cannot meet licensing standards will exit. Conservative estimates suggest 15–25% of current providers will not qualify or will choose not to invest in compliance. That is not a rounding error — it is a quarter of your addressable market disappearing.

The survivors consolidate. Licensed operators will absorb displaced demand. Chains and multi-site groups with compliance infrastructure already in place will gain share. Independents who invest early will be rewarded. The rest will merge, sell, or close.

KAM coverage models break. If your territory plan is built around 500 accounts and 120 of them vanish, your call cycle, your segmentation, and your incentive structure all need rebuilding. The commercial directors who start planning now will have a six-month head start on those who wait for the legislation to land.

The commercial move

This is not a "wait and see" moment. The smart play is threefold:

First, segment your accounts by licensing readiness. Which of your current accounts already meet likely licensing standards? Which are investing to get there? Which are not? That segmentation tells you where to concentrate resource now, before the shakeout.

Second, reweight territory plans toward licensed-ready operators. The accounts that will survive regulation are the accounts worth investing in. Shift coverage, shift incentives, shift your definition of a priority account.

Third, build relationships with the chains and groups that will consolidate. Post-licensing, the acquirers will be the power buyers. Getting in early — before they have absorbed three competitors and hired a procurement team — is the difference between partnership and tender.

The bottom line

Licensing regulation will compress the UK aesthetics provider base, accelerate consolidation, and force every manufacturer to rethink how they go to market. The commercial teams that treat this as a planning event — not a compliance event — will be the ones still growing on the other side of it.

The data is already in Rare.Monitor. The question is whether your commercial plan reflects it.